Written by Squareknot CEO, Patrick Schilling.

Australian sport was facing headwinds well before Covid-19. Covid-19 simply blew away the cloud cover of complacency that comes with legacy, the over-reliance on live content and the co-dependency between sport and broadcasting.

Life’s universal truth was forgotten – everything changes.

Beyond the introduction of the sale of broadcasting rights in the 1970s, the business of sport hasn’t changed in 100 years. It still survives on corporate sponsors, memberships, ticket sales and merchandise…all reliant on live sport.

The pandemic has exposed how ill-equipped clubs and codes are. From finances and commercialisation through to content and fan engagement.

While competitions are slowly returning, to survive, the business of sport must adapt.

Volatility creates opportunity. Crisis has a way of revealing talent, ability and mettle. It also provides opportunity to clean out those that possess none.

Everything Changes

ROI VS EGO

The days of ego-driven corporate sponsorships are fading. The lack of urgency in delivering ROI back to sponsors is well ingrained across sport in the same way gyms accept money from members that pay but never come.

As the Head of Digital at one AFL club put it, “We don’t look at sponsors’ ROI. They get to put their logo on our jerseys. If they’re not happy, we’ve got 15 other brands ready to take their place”.

If that sounds complacent, it’s because it is. If it sounds unsustainable, it will be.

Promotional spend is the first corporate cost lever to be pulled in uncertainty. In an increasingly data-driven economy, marketing spend that’s not discretionary, traceable or accountable is becoming an endangered species.

As promotional budgets shrink, clubs are at risk of forgetting that their greatest competition for corporate sponsorship is not another club but other media and platforms with better understanding of audiences and ways to connect brands with them.

With no live sport, clubs struggled to create engaging content to fill the void let alone create new revenue streams. Some leveraged Twitch to experiment with eSports but few built material audiences or found ways to monetise the channel.

Show me the money, please!

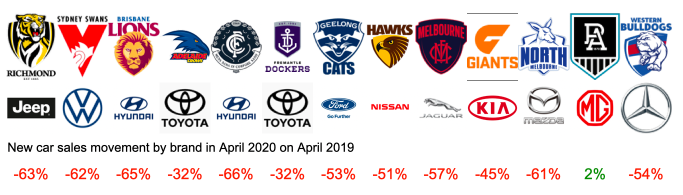

Corporate sponsors may have bigger problems near term than ROI from their sporting partnerships. Consider the AFL. The code, as well as 13 of its 18 clubs, are sponsored by major car companies. It’s hard to find a code anywhere so over-represented in sponsorship by a single industry.

Covid-19 has hit the auto sector like a perfect storm. Local new car sales fell 49% in April. Overseas, they were down 80-98%. The car rental industry which accounts for 10% of new car sales, has also taken a hit. Airports, where 1/3 of rentals take place, remain silent. Operators are selling down their fleets of cars while Hertz, Melbourne Demons’ partner, filed for Chapter 11 protection.

Beyond direct sponsorship of the AFL, it’s worth remembering that the auto industry spends $1.5bn per year on new car advertising in Australia. It is the biggest advertiser on TV. More on those implications later.

Some of the other large AFL sponsors under pressure include Virgin and Host Plus.

Virgin has gone in to voluntary administration. The list of potential buyers has fallen from 8 down to 2 at time of writing. Virgin is the partner of West Coast, Greater Western Sydney, Gold Coast, Carlton and Port Adelaide.

Host Plus‘ 1.2million members from the hospitality sector were hit first and hardest from the lockdown. They’re likely to be amongst the most active in regards to accessing their super and most vulnerable in the event of a second shutdown. Host Plus is the partner of Richmond and the Gold Coast.

The idea of a partnership loses its ammunition when benefits are unilateral. Now is when clubs should be approaching their partners with a clear message, “How can we help?“. Clubs have the audience, the reach and the content to create value for partners by helping in the form of PR, advocacy, awareness, branding and conversion.

In reality however, it’s hard to find mentions of corporate sponsors and partners on the social channels and digital content of any club, code or athlete. An opportunity lost.

Peak Broadcast Rights

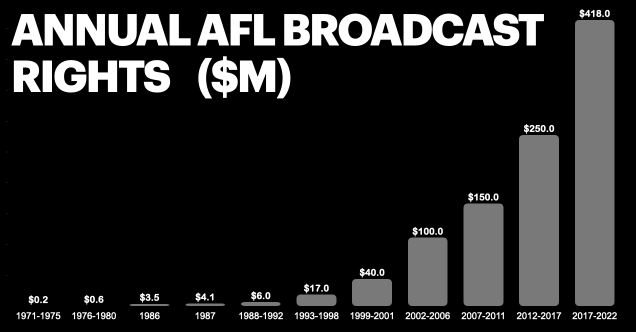

Australian sport lives and dies on broadcast rights. Before Covid-19, the sale of broadcasting rights of the top 6 codes were generating $1.4bn of revenue per year.

For the buyers, it means generating at least $1.4bn of advertising or other commercialisation opportunities. A tough ask in a good year let alone in a pandemic.

Sporting rights including the Olympics, the World Cup, EPL, AFL, etc, are often seen as a loss leader. A means to attract broader audiences in the hope that they will hang around and watch other content on the network. The cost/benefit equation however, is increasingly skewing to the earlier.

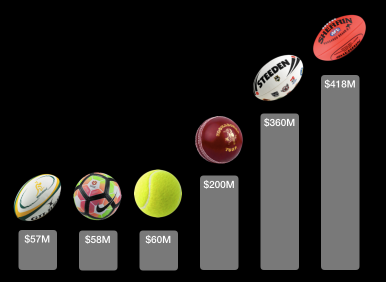

No rights have seen greater appreciation in value than the AFL. Such is the co-dependency between free-to-air/ pay-TV/ subscription services and leading sports.

In 2015, Seven West Media (SWM), Foxtel and Telstra agreed to pay $2.5bn for the AFL broadcast rights between 2017 and 2022. The new contract was a 100% mark up on the one it replaced.

Like any good Ponzi scheme, the appreciation of broadcast rights works until there’s no next sucker. Has Australian sport reached peak broadcast rights?

When these contracts were last negotiated, it was a different world. Everything changes.

In 2015, SWM was a $1.3bn multimedia powerhouse. Today, SWM is a $160m micro-cap, counting the cost of lost content, with limited access to capital, actively selling assets including magazines, production, radio and possibly its rights to the Olympics in a bear market to service over $500m of debt.

Foxtel’s revenues are continuing to decline as it faces accelerating churn, pricing pressure, cannibalisation from its own streaming services, a $2bn of debt and write downs. Foxtel’s major shareholders have continued to inject capital in support but even before Covid-19, News Corp and Telstra wrote their investment down by $1.7bn.

Such is the reliance on live sport that Foxtel and Nine have just renegotiated the rights for the NRL for $1.9bn. This at a time when Foxtel is cutting 200 jobs and standing down a further 140, News Corp is closing print editions of its regional papers and Nine is cutting costs by $100m.

Add to that, TEN is tightening its purse strings and seemingly no longer focused on sport. It currently has no Head of Sport.

In that environment, it begs the question of who will pay up for the next round of sporting rights? The cash pool is dwindling, key stakeholders appear increasingly less solvent and pricing tension has all but dissolved. We await eagerly imminent news of the AFL’s negotiations.

At best, codes should hope for flat outcomes in terms of value. In reality, even flat outcomes in terms of dollar value will be at the expense of longer terms. After all, these contracts are being renegotiated in a fast moving environment amidst unprecedented uncertainty.

The Way Forward

Think like an agency. Clubs are the gatekeeper between audiences and brands. Content is the lever. Understand the audience. Create the right content for the right audience on the right channel at the right time and monetise both audience and brands. Then monetise.

Understand your assets.Stories about sport are often more gripping than the sport itself. The real drama lies in the untold stories behind the journey. Look no further than the reach and appeal of The Last Dance docu-series. It extended far beyond just fans of basketball. In the process, it helped the audience of the NBA grow during the lockdown. Now look at what The Drive To Survive has done for F1, Sunderland Til I Die for English soccer, The Test for cricket…Codes and clubs are no longer just sports administrators. They’re media and entertainment companies sitting on phenomenal content sitting idle, waiting to be told.

No one owns the audience. Codes traditionally sell the rights to broadcasting, images, digital, merchandise, ticketing and catering. No one, however, owns the audience. Smarter clubs understand the value of mobilising, engaging and monetising fans. This is arguably where clubs can create the greatest incremental returns with full discretion. This is where technology + content + insight meet.

Dunning Kruger Effect. Too often, professional clubs still feel like they’re being run by volunteers. It’s quickly evident where ability parts company with a LinkedIn profile. If clubs are investing in their future, they must start with the right people. Uncommercial individuals in key roles are amongst the greatest threats to clubs.

Be of value. To fans. To staff. To partners. There is no consumer with greater brand loyalty than the sports fan. From birth to death. Sport is in a unique position of bringing people, content and brands together to create unique experiences and value for all stakeholders. Some are just not that good at it yet.

Doing nothing is not an option. Fans of VFL/AFL saw the repercussions in the 1980s and 90s. In this environment, the last thing fans want to see is the resurfacing of discussions around club relocations and mergers. But that’s another story. To understand that impact, keep an ear out for the upcoming podcast series No Merger.